Risk Off, Risk On, Kick Off & Lift Off

In a week where markets struggled to choose a single dominant theme, sticky inflation, Middle East War risk and the SpaceX mania float all took turns at the wheel. Yet for all the noise, major indices ended the week with a familiar reminder that even AI enthusiasm and trillion-dollar IPO excitement cannot fully escape the pull of inflation, bond yields and central banks.

The macro backdrop gave investors little room to relax during the week, as central banks and inflation moved back to the centre of the market narrative. In Europe, the ECB raised interest rates by 25 basis points, taking its rate to 2.40%, signalling that policymakers were no longer willing to simply look through the latest energy shock. The move was driven by continued inflation pressure from higher oil and gas prices, with the ongoing Middle East conflict increasing the risk that elevated energy costs feed further into the supply chain, corporate margins, and wage expectations. It left investors facing an uncomfortable mix of weaker growth expectations and tighter monetary policy.

The US inflation print added to the same concern. Headline CPI rose 0.50% in May and reached 4.20% year-on-year, with energy accounting for the bulk of the monthly increase. Shelter and food costs also continued to rise, while core inflation was more contained, but not soft enough to take pressure off the Federal Reserve. With investors already nervous the immediate reaction was higher bond yields, rate cut expectations pushed further out, and pressure on growth stocks, particularly semiconductors.

Tensions in the Middle East have fuelled the inflation fire and remained a key driver throughout the week. The week began with a fragile pause in hostilities, as Iran and Israel appeared to halt direct strikes following pressure from President Trump. However, markets remain uneasy, despite assurance from the White House that the US and Iran are close to a peace deal.

The caution proved justified by midweek, after reports that a US helicopter had been downed near the Strait of Hormuz, prompting fresh US strikes on Iranian air defence, radar, surveillance, and communications targets. Iran responded with missile and drone attacks on US-linked bases across the region, although US officials suggested the damage was limited.

By the end of the week, however, the tone had shifted sharply. With investors looking for any excuse to stay ‘risk on’ ahead of SpaceX’s International Public Offering (IPO), President Trump stepped back from threatened further strikes as diplomatic talks appeared to gain momentum, triggering what markets refer to as the TACO trade (Trump Always Chickens Out).

Gold’s reaction was more nuanced. Rather than behaving purely as a classic safe-haven asset, it was caught between geopolitical demand and the inflationary impact of higher oil prices, which risks keeping interest rates higher for longer around the globe.

Whilst commodities have made headlines for multiple reasons over the past twelve months, this week more interest is in beer consumption. As the Soccer World Cup kicks off, analysts expect football fans to drink an extra one billion pints during the tournament, a welcome boost for a brewing industry still grappling with cost inflation, softer demand, and shifting consumer habits. This year’s expanded format of 48 teams and 104 matches is expected to make it the booziest World Cup in history, with global sales volumes forecast to rise meaningfully over the 39-day competition.

The bigger story sits behind the pint! Carbon dioxide is used as a critical input to carbonate lager and beer and keep production flowing. With pubs preparing for a surge in demand, the UK government is launching a renewed push to strengthen domestic carbon dioxide supply, following repeated interventions in recent years to prevent shortages.

So, while oil and precious metals may dominate headlines, the World Cup offers a timely reminder that even the humble pint relies on a functioning supply chain, and that carbon dioxide resilience may be just as important to the national mood as whether the football world cup is coming home or not!

At company level, SpaceX dominated the week and especially Friday’s trading session. The largest IPO in history turned Elon Musk’s private space giant into a public market colossus, pulling much of the wider AI, semiconductor, and space-related ecosystem into its gravitational field. The Company priced at $135 per share, raising a record breaking $75bn, surged to a premium of 19% on debut and pushing its valuation above $2.1 trillion. The move lit up retail chatter whilst crowning Musk as the world’s first trillionaire.

For investors, the cleanest part of the SpaceX story remains Starlink, with more than 10 million subscribers across 160 countries. But the IPO is far broader than satellite broadband alone. It brings together launch dominance, Starship, xAI, orbital data-centre ambitions and a substantial Musk premium. The knock-on effects were felt across related names, particularly chip manufacturers and of course the impending AI IPO pipeline of OpenAI and Anthropic.

Looking to the week ahead, aside from England’s opening group game on Wednesday against Croatia, central banks take centre stage this week, with the Fed, Bank of England and Bank of Japan all due to announce rate decisions against a difficult backdrop of geopolitical tension and higher energy prices.

The focus will be the Federal Reserve, as Wednesday marks Kevin Warsh’s first meeting as Chair. Markets are still debating whether he leans hawkish or dovish, and if the Committee decide to adopt a more neutral stance from that of its existing easing bias. More importantly, markets will be holding their breath to learn whether the planned memorandum of understanding between the US and Iran does indeed become reality on Friday.

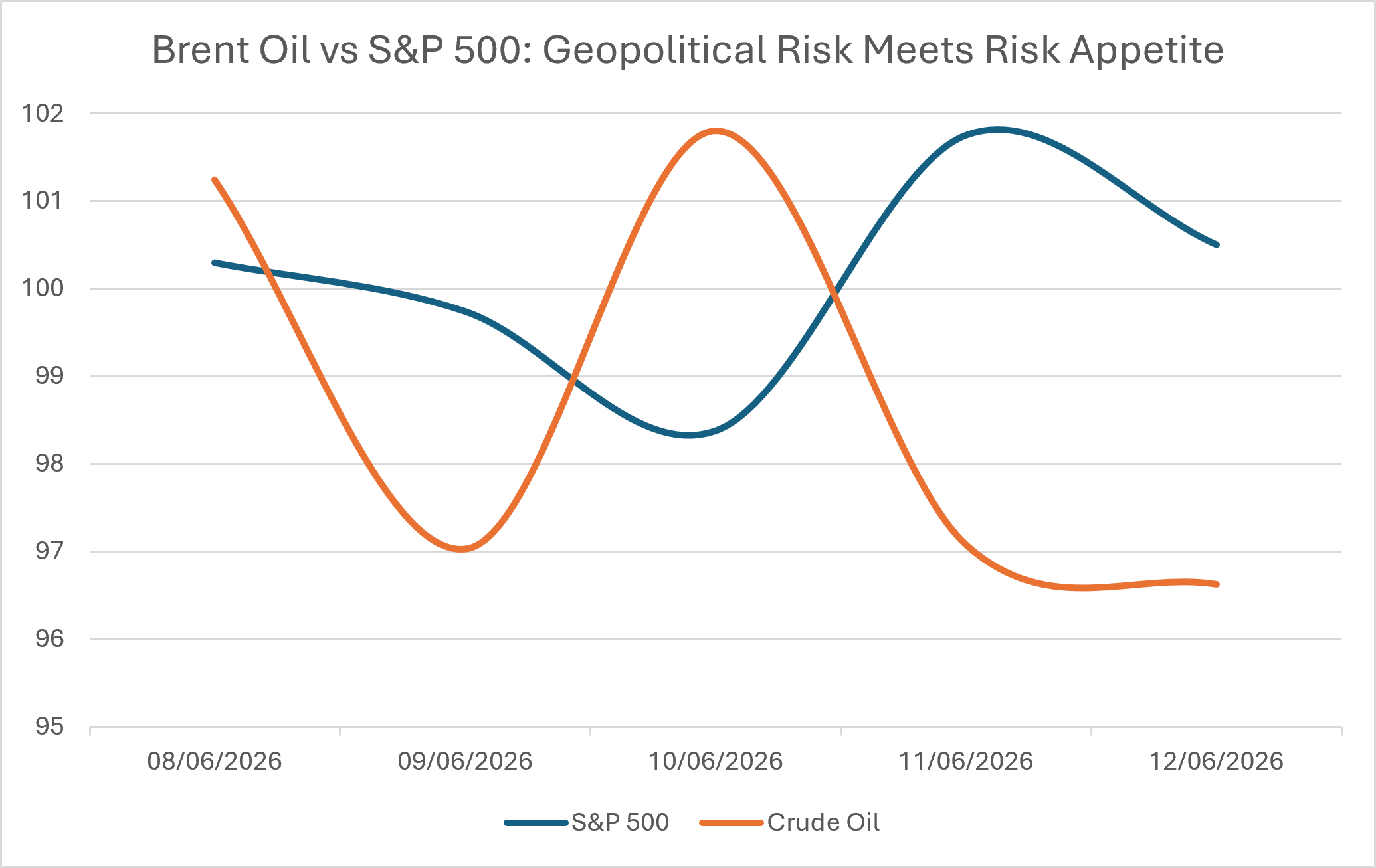

Chart of the week:

(source: Bloomberg, TEAM – prices rebased too 100)

Middle East tensions pushed oil higher midweek as investors priced in risk premium, while equities came under pressure from hotter inflation and rising bond yields. By Friday, de-escalation hopes, the “TACO” trade and SpaceX IPO enthusiasm helped risk appetite recover, leaving the week as a neat illustration of how geopolitics, inflation and sentiment pulled markets in different directions. TEAM’s exposure to both crude oil and the S&P 500 highlights the role of diversification, with different assets able to provide different return profiles during periods of volatility and market stress.

(Cover Image Source: SpaceX)