A Hawk, a Truce, and Trouble at Home

Global financial markets were handed no shortage of drama last week yet ultimately chose optimism over alarm. A record-breaking IPO, a hawkish Federal Reserve debut, a divided Bank of England, and the most consequential geopolitical development since February all collided in a shortened trading week for US markets.

The defining macro development arrived, once again, from the Gulf. The United States and Iran finally advanced an interim peace framework, setting in motion the reopening of the Strait of Hormuz, a route critical to global oil flows. Markets responded immediately, putting a bid under import-dependent economies including Japan.

Brent crude fell sharply into the high $70s, retracing much of the earlier conflict-driven spike and prompting a reassessment of how far the spring energy shock will continue to feed through to inflation.

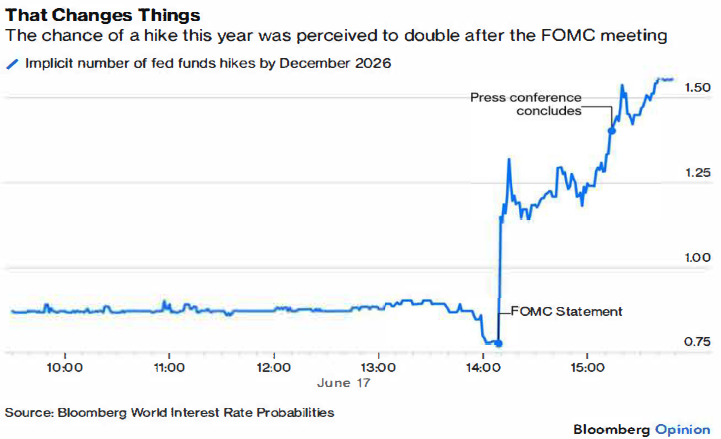

That shift matters for prices at the pump in the short term, but markets were reminded of the delicate balancing act facing central bankers as Kevin Warsh chaired his first FOMC meeting in America. Rates were held at 3.50%–3.75%, but the tone was unmistakably hawkish: the widely dissected press release was sharply cut, forward guidance removed, and projections moved from implying cuts to signalling that hikes remain firmly on the table.

Acknowledging the Fed’s dual mandate of maximum employment and price stability, the message was unambiguous: unlike his predecessor Jerome Powell, the Warsh Fed is prioritising inflation credibility, even at the expense of near-term market comfort.

It was a busy period for monetary policy decisions. The Bank of Japan raised rates to 1.00%, its highest level in three decades, pressing ahead with normalisation. Closer to home, the Bank of England held at 3.75%, but with a widening 7–2 split as two members backed a hike. The common thread is clear: the bar for easing is rising, not falling.

In the UK, the policy backdrop is being complicated further by the ongoing narrative of Labour government infighting. Pressure on Prime Minister Keir Starmer to step down accelerated markedly following Andy Burnham’s impressive victory in the Makerfield by-election.

What stands out most is how differently markets are interpreting the same set of facts.

Bond markets are signalling discipline, caution, and the spectre of inflation risks ahead. The move higher in shorter term yields reflected not just the rate decision, but a shift in how the Fed intends to operate. Gone is the language of reassurance; in its place is brevity, ambiguity, and a renewed emphasis on inflation credibility.

Equities, by contrast, remain focused on growth, liquidity, and the enduring pull of the AI theme. High profile company SpaceX is squarely at the centre of that tension. It’s Nasdaq debut, the largest IPO in history, prompted a wave of ETF index and retail investor flows, sending its valuation surging. The story highlights how flows, rather than fundamentals alone, are an increasingly important factor in driving index returns.

Price action in the commodities sector told the cleanest story. The prospect of restored flows through the Strait of Hormuz represents a meaningful reversal of the supply shock that has defined much of this year.

Gold moved in the opposite direction, falling on the back of a stronger dollar and higher real yields, a reminder that even safe havens must contend with the opportunity cost of rising rates. Industrial metals were more mixed, balancing improved growth sentiment against currency headwinds.

In summary, five forces defined the week. SpaceX reignited the debate over valuation and the power of passive flows. Warsh signalled a sharper, more hawkish Fed. The Bank of Japan tightened further, while the Bank of England held under growing internal pressure to move. Political uncertainty added a UK-specific layer of complexity. And, above all, the US-Iran agreement, however fragile, removed the single largest macro headwind weighing on inflation and sentiment since February.

Whether equity market optimism proves durable will depend on two factors: first, whether the reopening of the Strait of Hormuz holds; and second, whether central banks look through falling energy prices and maintain their tightening bias.

For now, investors have chosen to believe the best news on offer. Summer markets, as ever, may yet have other ideas.

Chart of the week

Markets interpreted Chair Warsh's first FOMC meeting as materially more hawkish than expected. Following the policy statement and subsequent press conference, investors sharply increased their expectations for additional rate hikes, with interest-rate futures moving to price in roughly 1.5 quarter-point hikes by year-end, about double the expectation before the meeting. The repricing reflected a perception that the Committee was prepared to keep policy tighter for longer in response to persistent inflation risks.