Quarterly Investment Review & Outlook

2nd Quarter Investment Review & 3rd Quarter Outlook 2026

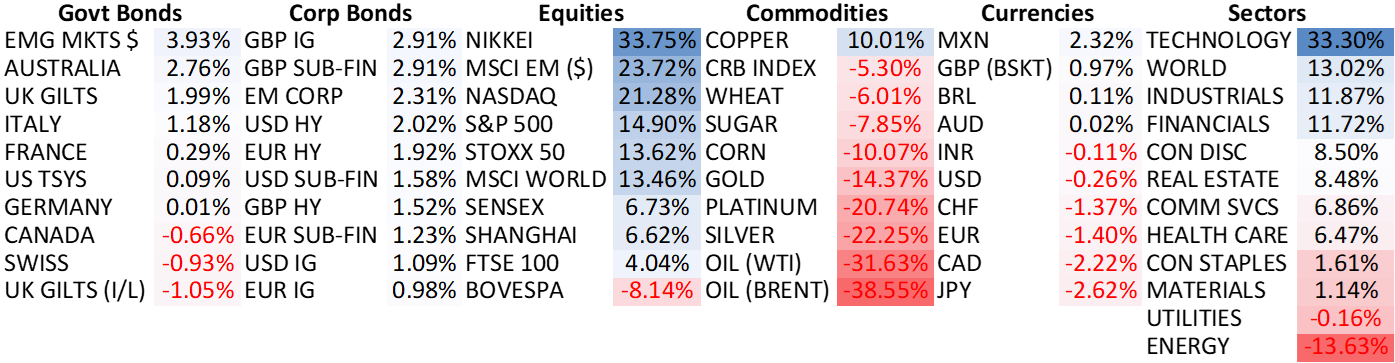

Major Asset Class Returns for 2nd Quarter 2026, GBP (£) terms

Investment Review 2nd Quarter 2026

Truce!

(Source: investing.com)

An extraordinary quarter that delivered one of the most powerful equity market recoveries in history, including a 9-week winning streak for the bellwether S&P 500 index.

Geopolitics and all things artificial intelligence (AI) remained centre stage. Breakthroughs in both themes took place against a backdrop of fragile investor sentiment caused by the ongoing hot war in the Middle East and healthy scepticism over whether AI-related capital expenditure plans from the so-called ‘Hyperscalers’ (Amazon, Google, Meta, Microsoft) were likely to culminate in meaningful profits for shareholders.

Following multiple false starts that included a brief reimposition of Hormuz restrictions by Iran, accusations and finger-pointing from both sides, and clear disagreement over the scope of any permanent deal, America and Iran, aided by Pakistani interlocutors, finally advanced an interim peace framework. The development followed thirty-eight separate threats by Trump to annihilate the Iran regime, or worse, all of which were subsequently walked back, underpinning the Donald’s ‘TACO’ (Trump Always Chickens Out) credentials.

Crude oil relief

A potential full reopening of the Strait was greeted warmly by markets. Oil prices tumbled, continuing their round trip to finish June at levels below where they were when the US-Iran conflict began. For context, the market has effectively priced a clean resolution to one of the largest geopolitical energy shocks in history, one that has seen the removal of more 1 billion barrels of oil from the market due to ongoing supply disruptions.

AI Mania

With the temperature around the Iran-US war cooling, the market’s attention (re)turned to corporate America, and crucial first quarter earnings season results and forecasts from C-suite executives at the world’s leading companies. The gnawing question on investors’ minds is whether the AI investment cycle is in danger of becoming one of the worst misallocations of capital in history.

Two distinct, but related, catalysts from the technology sector allayed those fears, at least for now. The first was the announcement of Claude Mythos Preview from Anthropic, its most capable AI model to date. Anthropic also revealed Project Glasswing, an initiative to deploy Mythos in securing critical global software infrastructure. Remarkably, Mythos was able to autonomously identify thousands of previously unknown, or overlooked, vulnerabilities across every major operating system released over the past four decades.

The second was validation from the earnings picture, personified by memory chip (the components that allow computers, smartphones, and AI systems to store and rapidly access data) maker Micron Technologies, which has taken the baton from Nvidia in arguably becoming the most important company in the world. Results and guidance from Micron are a real-time barometer for the health of the AI investment boom.

Bulls rejoiced following one of the biggest beats in semiconductor history. Top-line revenue of $41.4 billion and gross margins of almost 85% translated to almost 365 million dollars of profit every single day of the quarter. Astonishing. Investors interpreted the news flow as vindication of the AI thesis. The major beneficiary was the global semiconductor sector that soared higher in price terms amidst a renewed wave of optimism around demand for AI hardware and associated supply chains.

Fed Chairman Warsh

Turning to monetary policy, newly crowned US Federal Reserve Chairman Kevin Warsh presided over his first FOMC (Federal Open Market Committee) policy meeting mid-June amidst plenty of fanfare. Interest rates were held steady at 3.50% - 3.75%, but the tone was unmistakably hawkish. The widely dissected press release was sharply cut, forward guidance removed, and projections moved from implying cuts to signalling that hikes remain on the table.

Towards the end of the month, Warsh’s rhetoric softened, thanks to another helpful development on the inflation front. Core PCE (personal consumption expenditures), the Fed’s preferred measure of inflation, increased +0.3% month-on-month in May, and +3.4% year-on-year. This remains far above the Fed’s stated 2% target, but markets had been bracing for a nasty surprise on the high side.

King of the North

Closer to home, former mayor of Manchester, and ‘King of the North’ Andy Burnham looks well positioned to succeed Sir Keir Starmer as UK Prime Minster, marking the 7th different leader of Britain in less than a decade. He has vowed to put energy, housing, water, and transport under ‘stronger public control’ and backs nationalising Thames Water. So far, markets remain unconvinced.

Equities: Scores on the Doors (all returns in sterling terms)

Developed market equities (represented by the MSCI World Equity Index) delivered a +13.5% total return over the 2nd quarter. The S&P 500 large cap index returned +14.9% whilst the technology-laden Nasdaq Index, powered by mega cap growth stocks and all things AI, delivered +21.3%. Japan’s Nikkei 225 Index finished the quarter top of the pops with a stunning return of +33.8%. Alongside all things AI, Prime Minister Sanae Takaichi remains determined to deliver on her pre-election promise of fiscal policy easing, evidenced by the ruling LDP’s (Liberal Democratic Party) proposal to significantly reduce the consumption tax on food and beverages, commencing in April 2027.

The MSCI Emerging Markets Index delivered a +23.7% total return, as capital continued to migrate towards the chief beneficiaries, or the picks-and-shovels trades, of the AI capital expenditure arms race. The world’s three leading memory maker beneficiaries are all headquartered in North Asia. To give some context to the price moves, stock market capitalisations for Taiwan ($5.15 trillion) and South Korea ($4.66 trillion) at the end of the quarter catapulted each country to the 5th and 7th largest in the global index.

China’s Shanghai Index returned +6.6% as investors largely ignore growing positive macro dynamics including a record trade surplus (reflecting the country’s dominance in global manufacturing) and a related ongoing boom in intra-emerging market trade (which now accounts for a bigger percentage share than developed markets). Whilst Beijing continues to reiterate its desire for the domestic market to replace the property market as the main source of wealth creation in the country, there is scant evidence this is happening, yet.

Fixed Interest

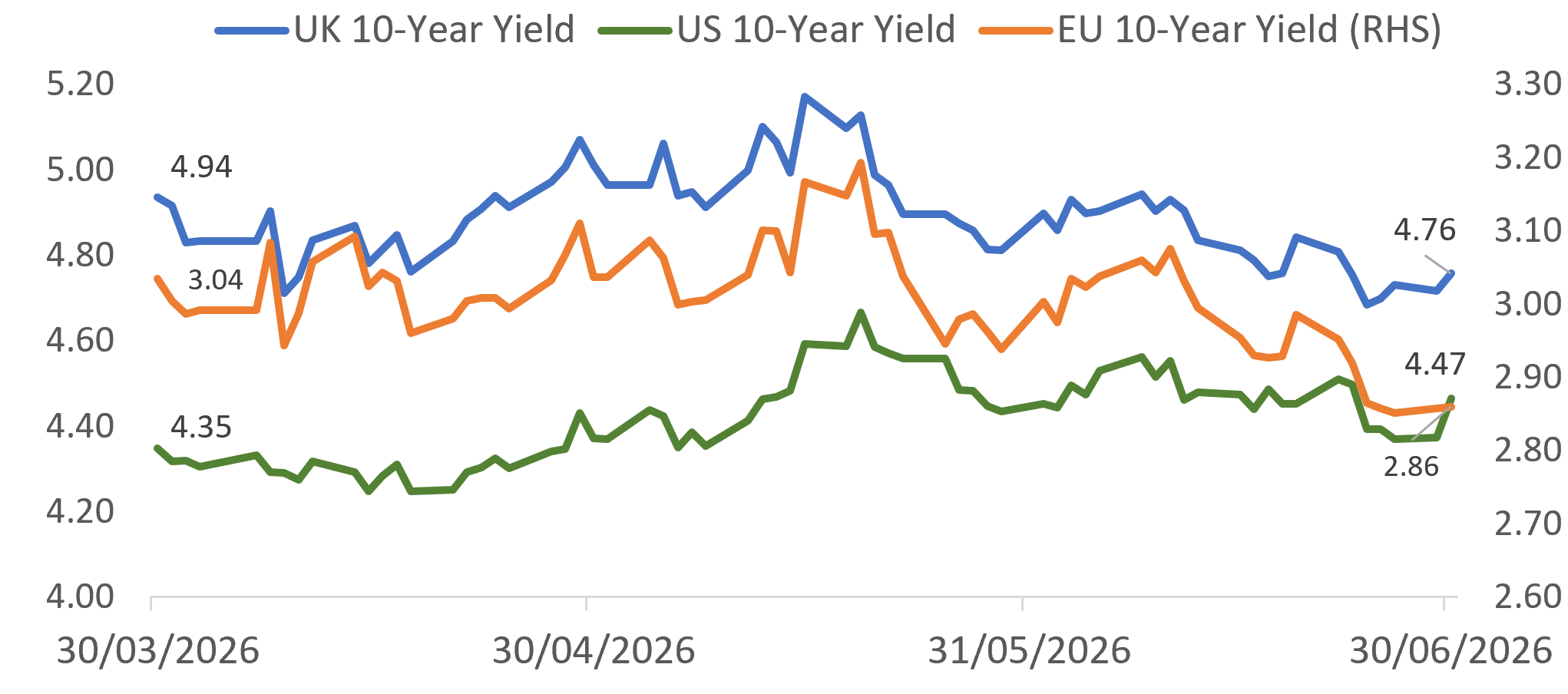

Government bond yields remained elevated throughout April and May as markets initially feared an extended shutdown of the Strait of Hormuz would force central banks to embark on rate hiking cycles to reduce the risks of the energy price shock feeding through to broader inflation.

Record debt government debt issuance also weighed on sentiment. More than $500 billion of sovereign bonds were issued in the first half of the year, more than in the first half of 2020 when nations were paying to support their economies during the Covid-19 pandemic lockdowns.

Budget deficits are widening again as governments boost military and infrastructure spending and more recently, to shield households and businesses from sharply higher energy prices.

Higher borrowing and higher yields are a toxic combination. Debt servicing costs now absorb over 19% of all US government revenues, a 40-year high. There is very little appetite from voters anywhere for fiscal conservatism and zero political strength from incumbent governments, to push through unpopular but desperately needed measures. These would naturally include higher taxes and/or lower spending, to put nations back onto a path of fiscal sustainability.

With that said, yields drifted lower during June as investors began to reassess the possibility of interest rate hikes across G7 economies. Catalysts ranged from softer-than-expected jobs numbers in America, anaemic growth prints in the UK and the EU, and worrying signs that individuals and households are feeling the pinch from materially higher everyday costs:

(Source: Bloomberg, TEAM)

ECB

As expected, the Governing Council of the European Central Bank voted unanimously to raise its deposit facility rate by a quarter of a point to 2.25%, the first hike since September 2023, and a sharp reversal from eight consecutive cuts delivered between June 2024 and June 2025:

(Source: Bloomberg, TEAM)

The decision was taken amidst the fog of war and reflected policymakers’ concerns that the energy price shock would trigger broader based price pressures, particularly in relation to wages. Flash Eurozone inflation hit 3.2% in May, the highest since 2023 and core inflation accelerated to 2.5% from 2.2% in April. The ECB raised its average inflation forecasts to 3.0% for this year and 2.7% for 2027.

President Lagarde was quick to assert that it wasn’t an ‘insurance’ measure, implying it is not a one-off hike. The Iran-US truce and reopening of the Strait of Hormuz, coming just weeks after the rate hike, has splintered opinion within the governing council. In one camp, there is the argument that tumbling oil prices back towards pre-war levels reduces the risks that there will be major second-order price effects. June’s sharp fall in headline eurozone inflation to 2.8%, and core inflation to 2.4%, gives further support to that view.

However, other policymakers, including Chief Economist Philip Lane, continue to warn that the inflation forces unleashed at the start of the conflict are still unfolding, and will take time to show up in stronger wage demands and delayed rises in food and services prices.

Federal Reserve

Under the stewardship of Chairman Kevin Warsh, the direction of Federal Reserve policy is also more uncertain. Warsh wasted little time signalling a distinctly different approach to his predecessors, and to make it clear that he will not be a stooge of the president who nominated Warsh because he expected lower interest rates.

When predecessor Jerome Powell was at the helm, the Fed missed its self-imposed inflation target for 63 straight months, reflecting a strong bias to the full employment side of its dual mandate.

In Warsh’s press conference following his first FOMC meeting, he referred to ‘price stability’ on a dozen occasions, describing persistent inflation as a burden on households. Markets unsurprisingly interpreted the development to mean that bringing inflation back down to target will be a much more important objective under his leadership.

Warsh has scrapped so-called forward guidance and set up five task forces to review the Fed’s $6.7 trillion balance sheet, communications (shorter, more direct statements), data sources (including how inflation is measured), productivity and the labour market (how AI and technology are reshaping the economy’s supply side), and inflation.

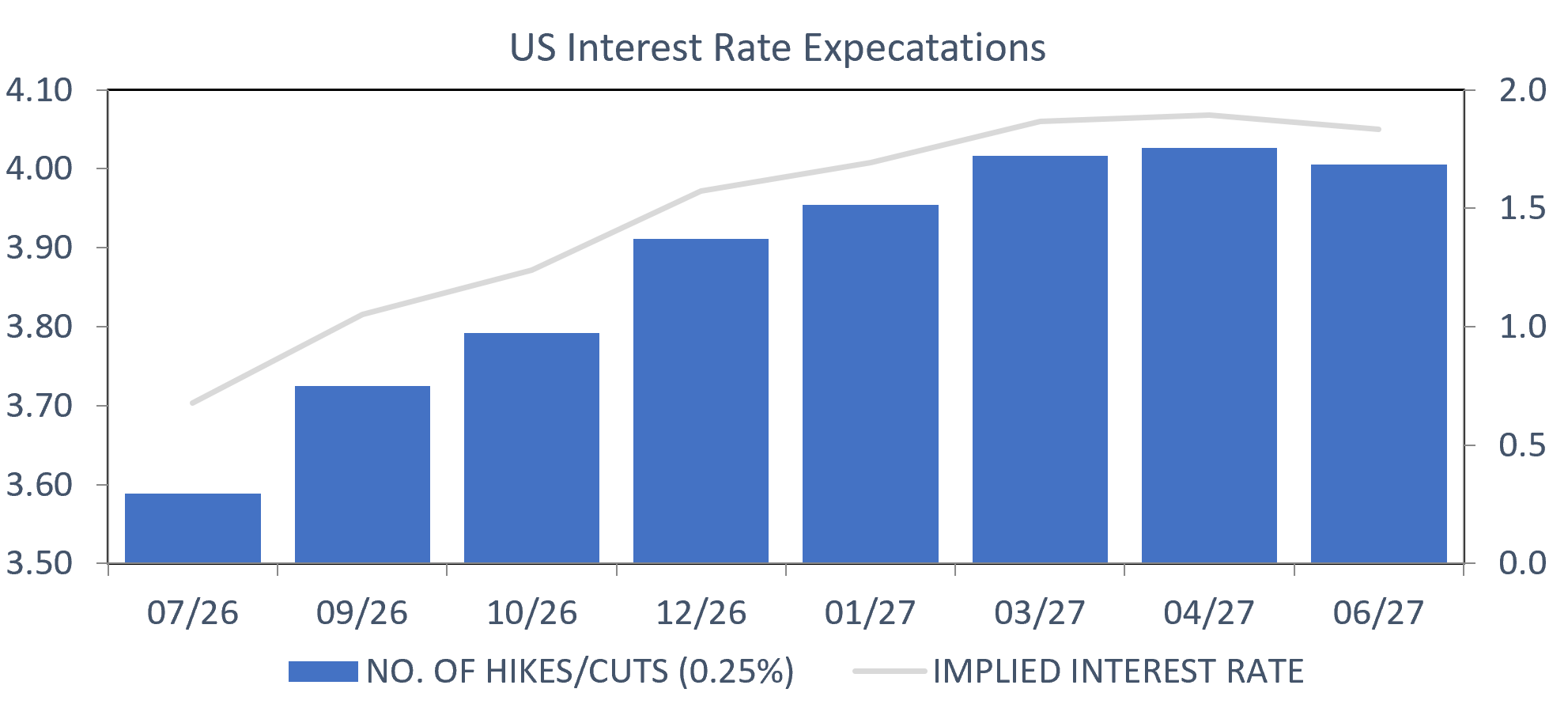

Whilst the FOMC unanimously voted to leave interest rates unchanged in June, the committee’s ‘dot plot’ revealed that nine of the 18 participants forecast at least one interest rate hike in 2026, and of those nine, six projected two or more hikes by year-end. The Chair did not submit his own dot, arguing that it can be over-interpreted by markets.

On the back of a red-hot nonfarm payrolls report for May, money markets had already shifted towards pricing in one rate hike over the next twelve months and following June’s FOMC meeting, are now pricing in the possibility of up to two hikes:

PHOTO (Source: Bloomberg, TEAM)

The end of the era of forward guidance seems to be catching on. At the ECB’s annual forum in Sintra there was a striking degree of agreement among the heads of central banks that trying to pre-commit to a future path for interest rates is less useful in world characterised by persistent supply shocks, geopolitical uncertainty and volatile inflation.

Christine Lagarde said that the ECB will move from forward guidance to ‘framework guidance’, explaining how the bank will make decisions rather that say what it will do next. The Bank of England’s Andrew Bailey and Tiff Macklem of the Bank of Canada expressed similar reservations over pre-committing to future policy, implying a broader change in central banking practice.

BOE

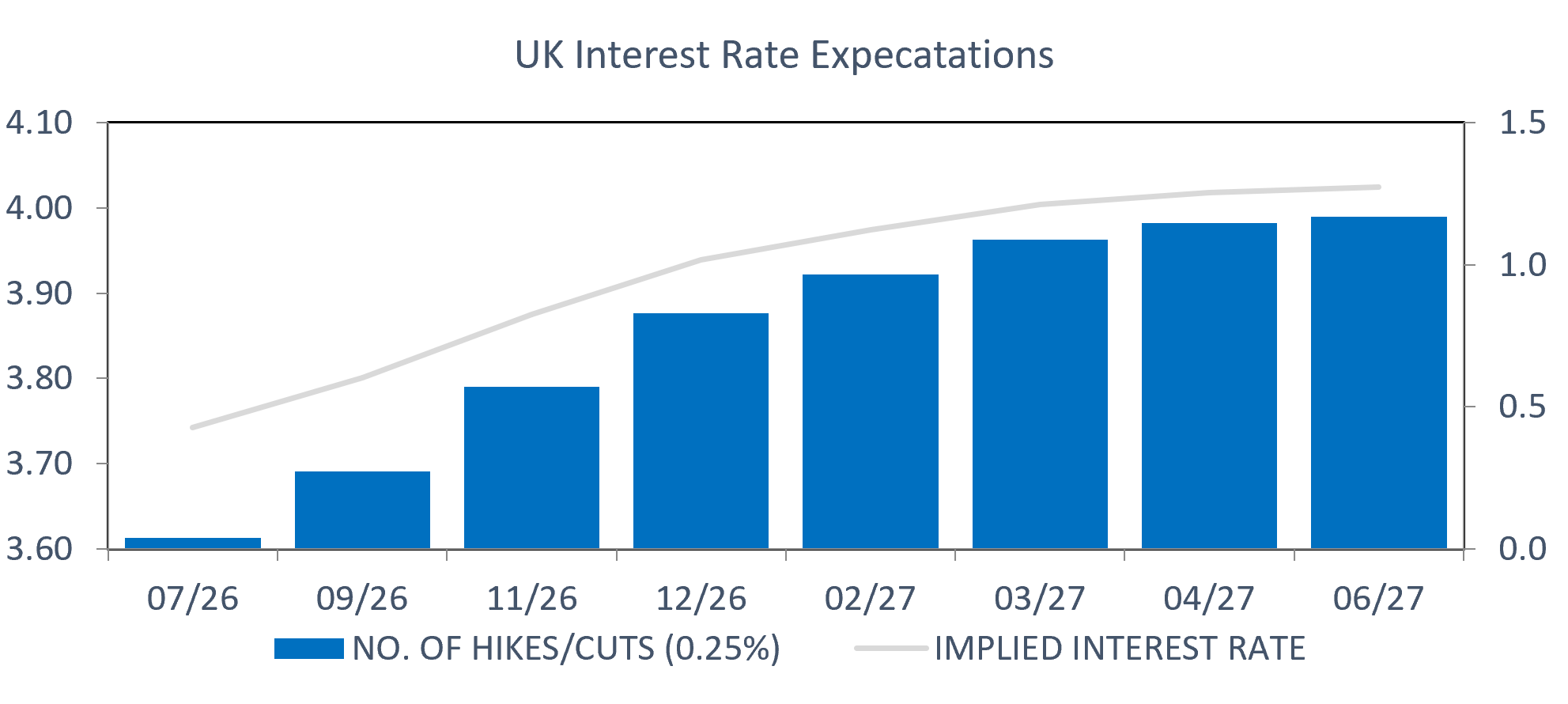

Closer to home, the Bank of England ultimately decided to keep interest rates steady through the quarter at 3.75%. The policy committee faces a delicate balancing act between inflation, which remains uncomfortably high, and growth that continues to disappoint. Whilst the US-Iran truce has helped alleviate oil and gas pricing pressures in the short-term, a 7-2 split over the rate decision suggests a degree of unease amongst voting members.

A minority, including the bank’s chief economist Huw Pill, called for an immediate quarter point increase to mitigate the risk of elevated energy prices feeding into wages and other prices. Conversely, the majority, including BoE Governor Andrew Bailey, are willing to tolerate the highest inflation rate in the G7 in the short-term due to the deteriorating economic outlook. The UK is forecast to expand at a sluggish +0.6% in the first half of 2026. Worryingly, the unemployment rate has climbed to the highest level since the pandemic.

Against this backdrop, money markets are projecting just one hike from the BoE over the next 12 months. Tumbling oil prices might give them cover to avoid tacking inflation more assertively:

(Source: Bloomberg, TEAM)

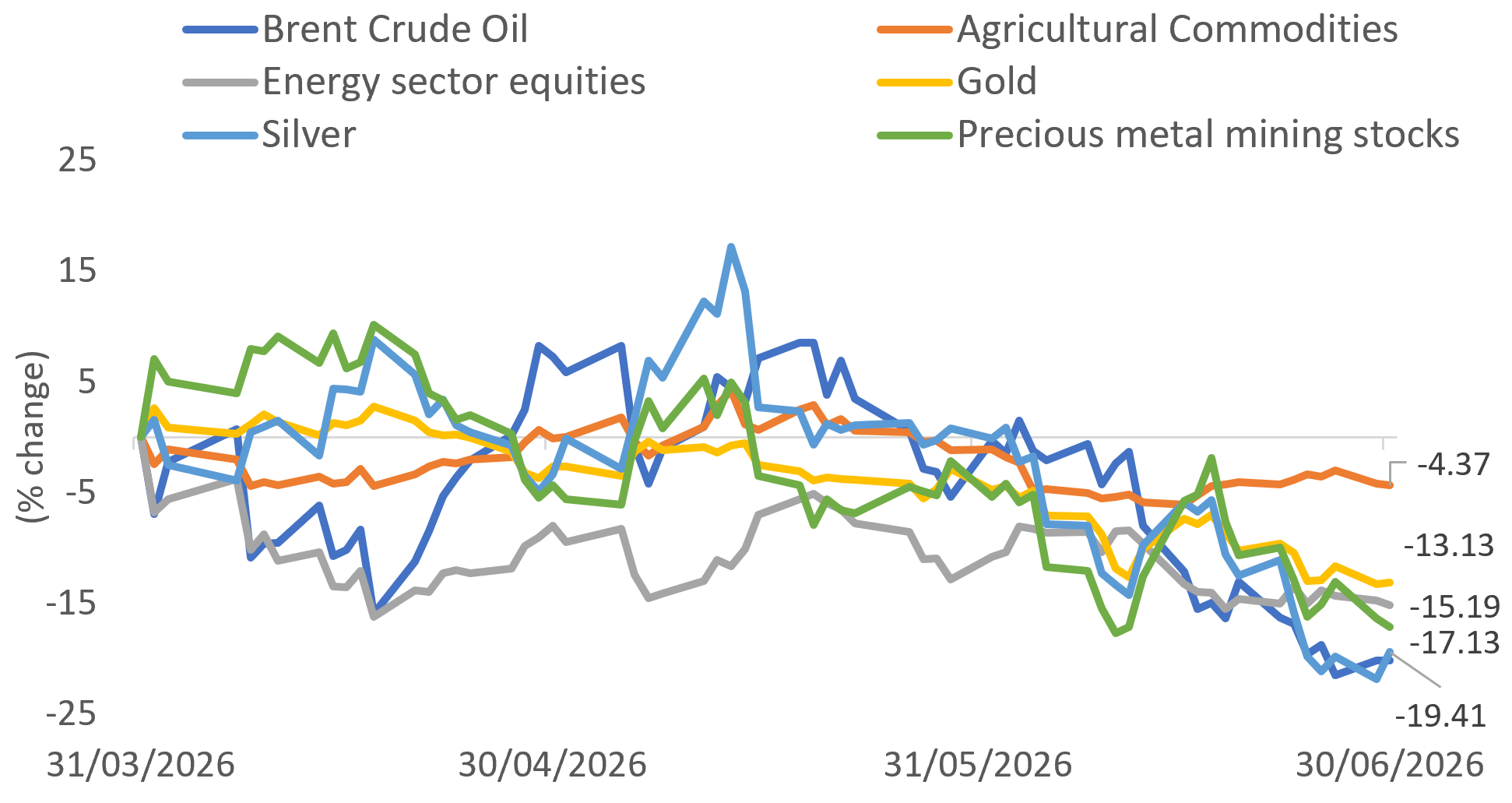

Commodities

Oil and gas prices

A complete reversal of the price action witnessed during the first quarter, as markets moved more aggressively to price in a swift return to ‘normal’ operations in the Strait of Hormuz. The truce terms included an agreement to keep the fully open with no external tolls, fees, or shipping charges being levied and a 60-day license that permits Iran to produce and sell oil to America. Investors firmly believe that the proverbial geyser will be unleashed over the coming months, leading to a global supply glut.

Gold & Silver

Precious metals prices remained in an air pocket this quarter with gold losing its shine amidst a range of fundamental (selective central banks cash-strapped and forced sellers of gold, real bond yields soaring providing an attractive alternative investment) and technical (leveraged ETF exposure unwind, retail investors panic-selling after joining the party late) factors.

Silver had a similarly turbulent ride. Her dual role: part precious metal, part industrial commodity, made it particularly susceptible to sporadic fears of an economic slowdown during the quarter, dampening industrial demand.

Precious Metals Mining Stocks

Precious metal mining stocks also suffered, with investors raising short-term concerns on two fronts. First, that the sharp drop in spot gold and silver prices would impact production prices for leading companies. Second, that sticky operational costs arising from high wages and residual energy expenses from the early-quarter oil spike would further squeeze profit margins.

Separately, within the institutional space, the phenomenal rally that the sector enjoyed into March would have made exposure a prime candidate for funding opportunities elsewhere:

(Source: Bloomberg, TEAM)

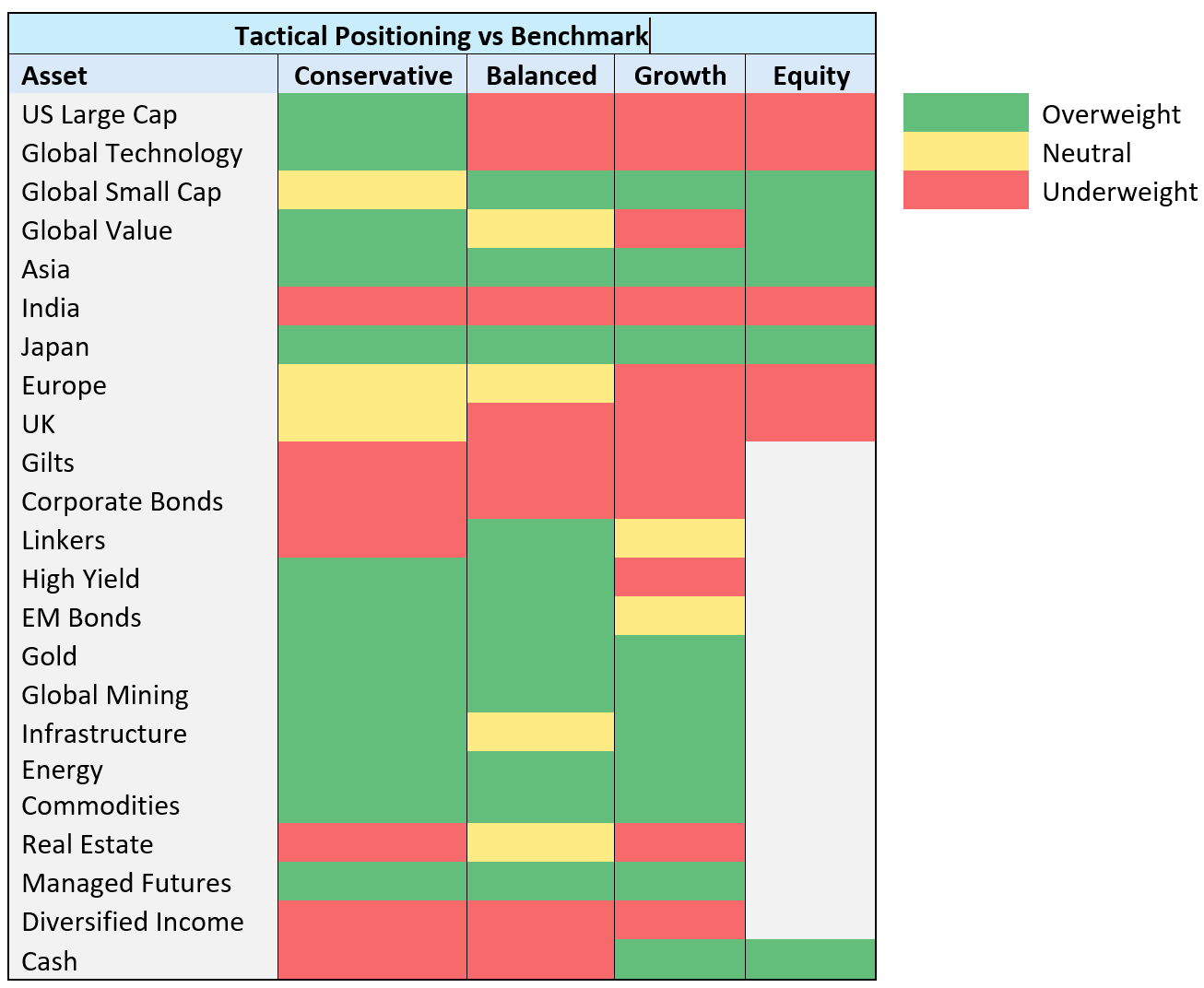

TEAM Positioning & 3rd Quarter 2026 Outlook

What worked during Q2 2026: American mega cap technology stocks, South Korea and Taiwan equities, value-orientated global equities, US infrastructure equities, Japanese equities.

What did not work during Q2 2026: Commodities, including physical gold, precious metal mining stocks, energy sector equities, and agricultural equities, cash, ultra-short duration government bonds.

As we enter Q3 2026, our asset allocation for the core TEAM MPS multi asset range and equity strategy is shown relative to neutral weightings in the table below:

Equities

Since Microsoft’s highly publicised $10 billion investment in Open AI (creator of Chat GPT) in January 2023, the AI theme has dominated the market narrative whilst exerting increasing influence on the composition and performance of major market indices from Asia to America. The potential profit pool is considered so valuable that it has prompted some of the biggest listed companies on the planet to alter their operating models, moving from asset-light to asset-heavy businesses in pursuit of AI supremacy.

A few developments are worth keeping a close eye on, in our view.

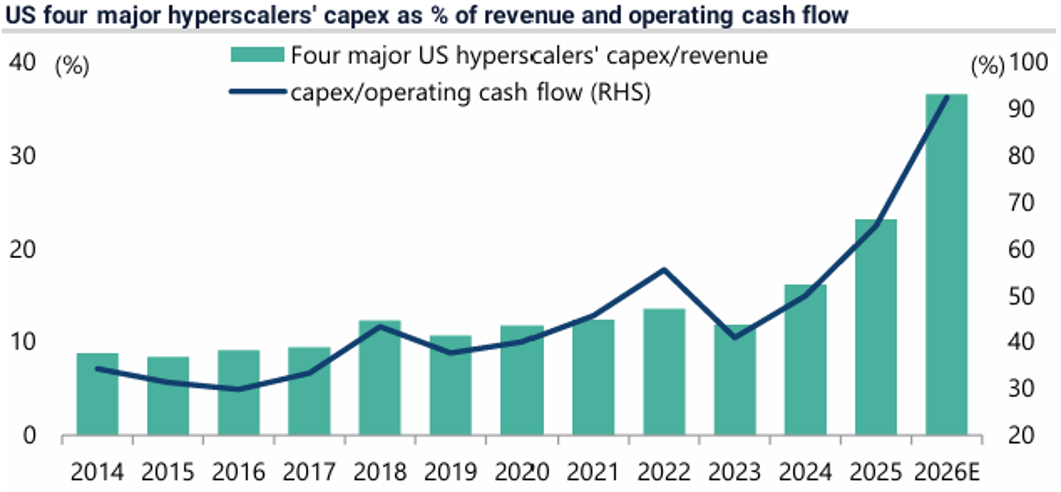

First, the market’s appetite, or lack of it, to carry on rewarding mega cap tech companies for spending gargantuan sums of money on AI-related technology. For reference, the four so-called hyperscalers, namely Alphabet, Amazon, Meta, and Google, are projected to spend a combined $800 billion on AI capex in 2027. Three key areas will receive the lion’s share of this budget: 1) powerful AI chips, 2) data centres to house supercomputers, and 3) power grid infrastructure to ensure that immense electricity needs are met.

From an investment perspective, the current AI capex cycle is akin to pouring an accelerant on a rapidly burning cash flow pile. According to the latest consensus cash flow estimates for the four hyperscalers above, capex as a percentage of operating cash flow has more than doubled in three years to 92% in 2026:

(Source: Bloomberg, Jefferies Global Research)

Second, insatiable demand for AI compute has driven prices of DRAM (Dynamic Random Access Memory) chips and tokens sky-high. DRAM chips offer super-fast ‘working memory’ that computers, smartphones, and servers use to hold data while actively running tasks. An AI token is a fragment of a word, image pixel, or genetic code sequence. When we prompt an AI, the data is chopped into tokens, and AI is billed, or measured, by how many tokens it consumes, or generates. Newer generations of each are more costly.

Taken together, the combined cost impact is already being keenly felt at the corporate level. Credible AI monitoring websites point to a growing trend: global businesses and tech startups are pulling their workloads away from expensive US cloud platforms and towards cheaper alternatives, threatening a massive wave of financial malinvestment for Silicon Valley. Investors, sensing that an attractive return on investment from this vast capex cycle is rapidly becoming a pipe dream, sold the hyperscalers aggressively.

Finally, we witnessed the real-world transmission mechanism from AI supply chain pressure to consumer prices. Apple CEO Tim Cook previously announced that price hikes across products were ‘unavoidable’ given the skyrocketing costs of AI memory chips, and the company duly obliged during June with sticker price increases of $100-$300 across Mac and iPad products. Could this be the start of another inflationary wave?

Fixed interest

The truce between Iran and the US provides some welcome relief for central banks, reducing immediate pressure on policymakers to raise interest rates when economies are slowing. However, whilst short-term rates are likely to be lower than feared just a couple of months ago, we do think there is a lot of complacency over inflation.

Although oil prices have rapidly faded back towards prewar levels, it will take weeks, if not months, for shipping traffic through the Strait of Hormuz to normalise and significantly longer to repair or rebuild production facilities that have been damaged or taken out of service.

We continue to see a risk of steeper yield curves and higher long-term rates as skewed to the upside due to the heavy supply of government bonds without the ongoing support of central bank buying. The ECB is operating in the other direction with its ongoing ECB quantitative tightening (shrinking the government balance sheet) programme.

Governments have responded to steeper curves by skewing issuance toward shorter maturities, but it is a short-term fix which will ultimately increases refinancing risk, especially increasing competition for capital from the hyperscalers. In a beauty parade, the balance sheet strength of big tech looks much more appealing than most governments.

Although credit spreads are at historically tight levels, we do not foresee a catalyst for meaningful widening and in a stable environment their excess carry of credit should underpin their outperformance and provide a buffer against volatility in government bond yields. However, tighter credit spreads leave less room for error and credit, and sector selection will be a more important driver of performance than in recent years.

Liquid Alternatives

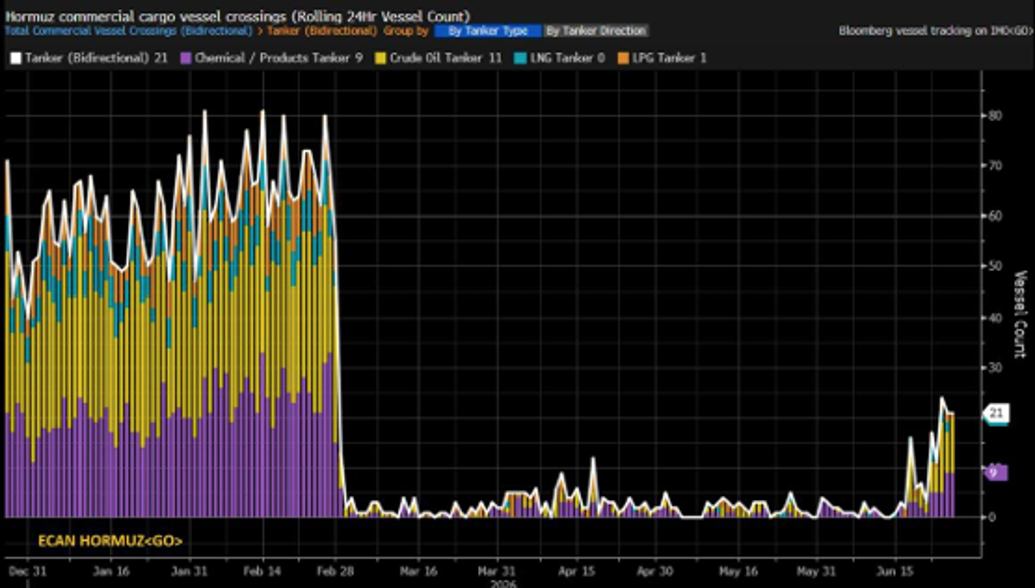

Amidst AI fever that gripped markets, geopolitics took a back seat last quarter. Stunningly, oil markets have roundtripped to below pre-war levels. The inference is that the war, in the eyes of the energy sector, never happened. The combined effect of deescalation, China (historically a big buyer at the margin) pulling back import purchases, SPR (Strategic Petroleum Reserve) releases by various governments, and ghost ships ushered through the Strait by the US blockade created constant downward pressure on oil and gas prices.

Nevertheless, it is worth bearing in mind that the still-fragile truce has been achieved via a Memorandum of Understanding (MOU), signed on 17 June. This is a preliminary framework designed to end the war between the two nations and is a temporary non-binding stepping stone rather than a final treaty. Given the track record of America, its allies, and Iran in maintaining so-called ‘deals’ over the past two months, stalled high-level talks, and Iran’s clear leverage over the Strait of Hormuz, flare-ups cannot be ruled out.

From a fundamental perspective, the global inventory picture is a reason to be less pessimistic about the outlook for oil from here. US refineries have been pushed to their production limits, with utilisation levels hitting multi-year highs, pushing crude oil inventory levels to five-year lows. In addition, SPR’s around the world will need to be replenished. Finally, commercial tanker traffic flow through the Strait of Hormuz. illustrates that activity has increased markedly from collapsed levels but remains at c. 20% of peak activity:

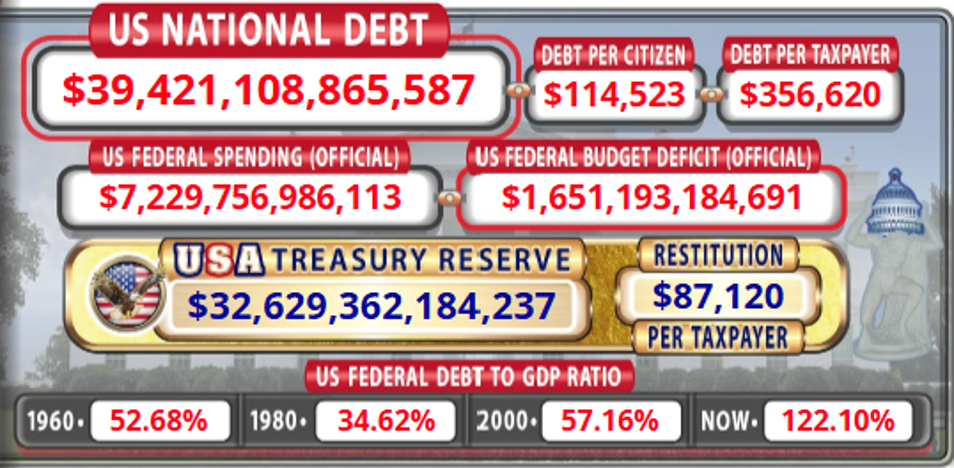

(source: Bloomberg) Turning to gold, the incumbent US government finds itself locked in a proverbial straitjacket regarding public finances. The brutal reality facing the US government is that approximately 93% of existing US interest payments are directed to Medicare, Medicaid, and Social Security, which are essentially ‘untouchable’. The fact that the enormous US debt mountain continues to grow despite a bumper federal tax revenue season which provided Trump and team MAGA with a huge cash influx speaks to the enormity of the challenge. Almost another 280 billion dollars was added to the national debt over the prior quarter:

(Source: USdebtclock.org) With politicians across G7 unwilling, and/or unable to make the tough choices required to address the growing global debt binge, owning real assets with no meaningful way to increase supply in the short term would seem to be a sensible approach. That extends to silver, and leading precious metal mining companies that are geared to higher longer-term spot prices.

Positioning into Q3 2026

Our preferred barbell approach of pairing US mega cap technology stocks with ex-US international markets to express the AI supply chain theme continues to lead us into the ‘memory makers’ including Samsung Electronics and SK Hynix in South Korea, in addition to chipmaker TSMC. In addition, we enter the third quarter strongly overweight Japan, a market that continues to attract strong international interest on the strength of its economic and corporate makeover.

Looking ahead on a longer-term basis, another leg to the AI story may be building. China has been quietly experiencing its own AI revolution. June witnessed the release of AI model GLM 5.2 by Hong Kong-listed Z.ai, which poses a severe threat to the dominance of America’s tech behemoths including OpenAI, Google, and Anthropic. This development (also bullish for established memory makers as chip demand explodes further) remains largely unrecognised by the international investor community.

In fixed income, we firmly favour a mix of ultra short government bonds (given our views on the potential for a secondary inflation wave and the growing G7 government debt problem) and good quality investment grade credits, focussed on the ‘belly’ of the curve, which are less exposed to any volatility in long-term rates but can also take advantage of steeper credit curves.

Our liquid alternatives sleeve remains a key differentiator versus benchmark and peer group. Here, our framework continues to indicate that real assets are become increasingly more attractive against a backdrop of growing global demand and supply shortages.

Elevated volatility and rising correlations (assets moving up and down in a similar manner) across our multi asset menu have also led us to hold healthy levels of cash for our lower and medium risk mandates. We anticipate that the summer months will provide a better opportunity to layer back into risk assets.

As always, rather than attempt to look around corners and predict outcomes, we rely steadfastly on our systematic investment process, which has successfully navigated an array of market conditions during this post-pandemic cycle and delivered respectable risk-adjusted returns for our investors.

Thank you for your continued support and interest in TEAM.

Craig Farley, Chief Investment Officer July 2026