Weak US jobs report boosts stocks

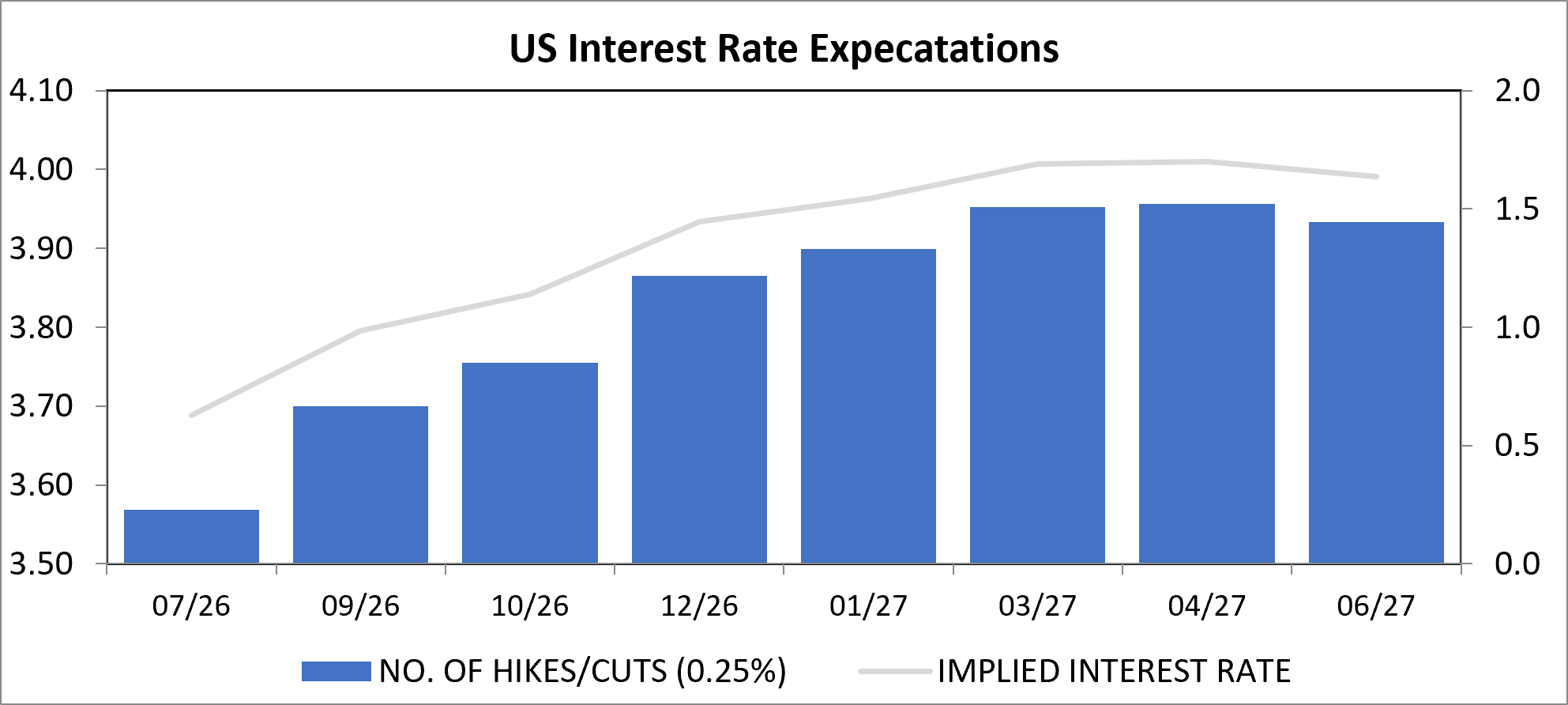

In a holiday-shortened week with US markets closed on Friday for Independence Day, risk assets rallied into quarter end gains as of a much weaker-than-expected US jobs report and more dovish rhetoric from the new Fed Chair Kevin Warsh pulled interest rate-hike expectations down.

The monthly Nonfarm payrolls report revealed just 57,000 jobs were added in June, well below the 113,000 expected, and the softest reading since February's negative print. Prior months were revised down too, May's gain cut to 129,000 from 172,000, April's to 148,000 from 179,000, while labour force participation fell to a five-year low even as the unemployment rate ticked down to 4.2%. The report was released a day early (Thursday, ahead of the holiday), and the market reaction was immediate: the probability of a July Fed rate hike dropped from around 29% to about 18%.

At the European Central Bank’s annual forum last week, Kevin Warsh softened the hawkish read markets had carried out of June's FOMC meeting. He told the forum that inflation risks had come down and notably declined to commit to a specific rate path, a shift that helped pull back some of the tightening expectations built up after June's more hawkish dot plot.

He also used the platform to push back on President Trump's pressure campaign against the Fed, insisting its independence wouldn't change regardless of political pressure, and previewed his broader institutional reform agenda, arguing the Fed has spent too much time trying to predict the future and should rely less on forward guidance and dot-plot-style forecasting.

The end of the era of forward guidance seems to be catching on. Christine Lagarde told the conference that the ECB will move to “framework guidance”, explaining how the bank will make decisions rather that say what it will do next. The Bank of England’s Andrew Bailey and Tiff Macklem of the Bank of Canada expressed similar reservations over pre-committing to future policy, implying a broader change in central banking practice.

In corporate news, Apple contributed to more volatility in tech stocks, driven by warnings around rising input costs, specifically a memory/DRAM chip shortage that's been squeezing margins across the industry. It has increased the price of MacBooks and iPads by about 20%, one of the broadest price rises in its history, due to the AI infrastructure’s boom that has caused the chip shortages.

A Kiplinger report published mid-week suggested Apple's recent price increases could be "a harbinger for a years-long era of costlier electronics" tied to this memory crunch. Apple was reportedly even looking at sourcing from blacklisted Chinese chipmakers to help address the AI-driven memory shortage pressuring its margins.

Shares in EasyJet were set to open sharply higher on Monday after its board agreed in principal to accept an improved GBP 5.5 billion takeover proposal (690p per share in cash) from US investment firm Castlelake. EasyJet’s share fell to as low as 360p at the start of the Iran war and the proposal will allow its founder, Sir Stelios Haki-Ioannou, to hold on to his family’s 15% stake.

In commodity markets, Oil prices declined after OPEC+ agreed to increase production from August, easing concerns that the recent Middle East conflict would result in a prolonged supply shock. Brent crude fell to $72 a barrel, its lowest level in almost four months. Although ship transits through the Strait of Hormuz have picked up, volumes remain well below the roughly 135 vessels per day that typically transited the Strait before the conflict. Many shipowners remain cautious because of lingering security risks, including mines, restricted transit corridors and the possibility of renewed disruption.

The price of gold briefly fell below $4,000 a troy ounce on Tuesday, rounded out its worst quarterly performance in more than a decade, on concerns of higher interest rates and waning enthusiasm among retail investors. However, Warsh’s more dovish outlook at Sintra drove a recovery back up to $4,178 at the end of the week.