Global financial markets weekly wrap

Geopolitical tensions rise.

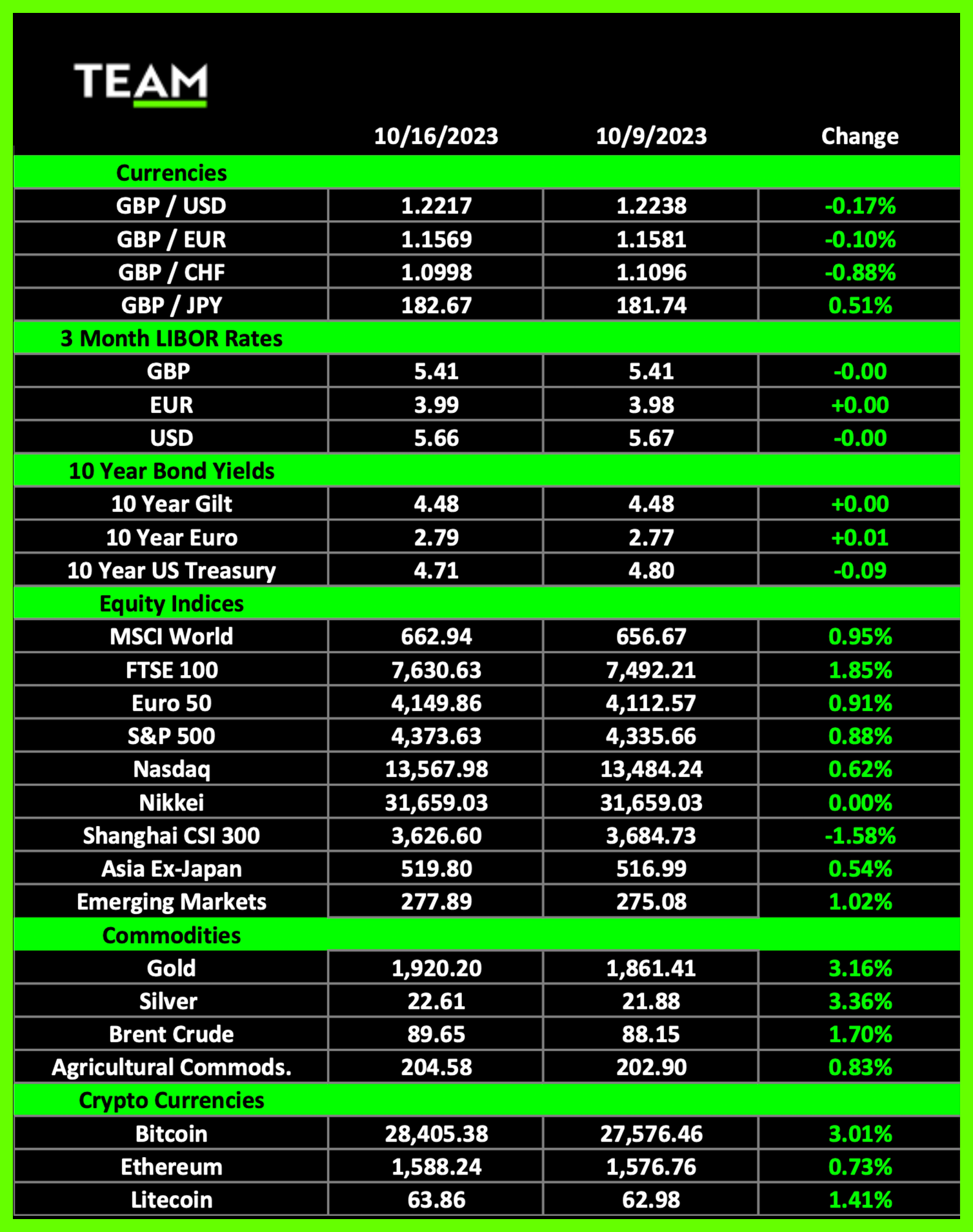

US equity markets finished this week slightly higher with the S&P and Nasdaq rising +0.9% and +0.6% respectively as investors weighed the renewed Israel-Hamas conflict and rising political tensions in the Middle East. A possible US government shutdown also remains on the table, with the current funding extension set to expire on November 17. The unprecedented recent ousting of Speaker of the House John McCarthy with no clear replacement has shaken already fragile confidence amongst the American people regarding the US political system.

Smaller capitalisation companies continued to struggle relative to their large counterparts. The Russell 2000 Index was down -0.5% and has now fallen approximately -14% from its high this year recorded on July 31. Investors seem to be taking the view that in a world of rising cost pressures and higher debt servicing costs, larger companies with balance sheet strength and access to bond markets offering more attractive lending terms are preferable at this stage of the cycle.

Separately, US data released during the week indicated that the inflation genie has yet to be bottled. US inflation expectations rose sharply from +3.2% year-on-year in September to +3.8% YoY in October according to the University of Michigan’s consumer sentiment survey, the highest levels since May 2023. The Core Consumer Price Index (CPI), a measure of changes in the price of goods and services excluding food and energy, rose +0.3% month-on-month, driven to a four-month high by rent and healthcare increases.

Nevertheless, markets were buoyed by comments from various Federal Reserve officials that pointed to a potential peak in US interest rates, with Lorie Logan, president of the Fed’s Dallas Bank, and Mary Daly, president of the Fed’s San Fransico Bank, both indicating that current restrictive monetary policy is helping to cool the economy. This softer tone led to a repricing of the need for an additional rate hike to less than 50%.

Turning to corporate America, the third quarter earnings season kicked off on Friday, as three major banks including JP Morgan Chase reported results, all exceeding aggregated analysts’ expectations for net income and revenue. Investors will have noted JP Morgan Chase CEO Jamie Dimon’s comments that ‘now may be the most dangerous time the world has seen in decades’, with concurrent wars in Ukraine, Israel and Gaza set to have far reaching impacts on ‘energy and food markets, global trade, and geopolitical relationships.’

In the commodities space, precious metals prices including gold were well bid on account of their haven status, and oil rallied strongly on escalating tensions in the Middle East and a strategic US move to tighten sanctions against Russian oil exports. US crude oil (West Texas Intermediate) was trading at $87 per barrel, up $4 on the previous week.

Looking ahead, a report on US retail sales scheduled to be released on Tuesday will indicate whether recent positive consumer spending momentum extended into September, whilst the weekly US jobs data has taken the baton from inflation in becoming arguably the most closely followed data point globally. On the corporate earnings front, Charles Schwab, Goldman Sachs, Bank of America, Johnson & Johnson, Tesla, and Netflix are among the companies reporting results this week. Impressive revenue and margin growth will likely be needed to justify current valuations.